The short version

A transfer agent keeps your shareholder records, issues and cancels shares, and pays out distributions. Almost no early-stage private company is legally required to have one. Delaware lets you keep your own stock ledger on a computer, in a database even, so we do.

- Most private startups are not required to use a transfer agent. The line (Securities Exchange Act Section 12(g)) sits at 10 million dollars in assets and 2,000 holders of record, not before.

- Your stock ledger is your record. DGCL 219 makes it the only evidence of who can vote, and DGCL 224 lets you keep it electronically.

- We keep ours as a JSON file in Git. AI does the reconciliation, the stockholder list, and the reports. A human and our counsel make every legal call.

- When do you need one? Going public, a Regulation A+ Tier 2 raise, or a Reg CF round where you want the holder-count exemption. Ask a securities lawyer about your facts.

A question that makes founders shift in their seats: who is your transfer agent? At Tallyfy, the answer is nobody. We run our own cap table. No transfer agent, no monthly cap-table subscription. A JSON file in version control, and AI doing the reconciliation a service used to bill us for.

Do you need a transfer agent? If you are an early-stage private company, almost certainly not. The law does not require one until you get much bigger, or until you do something specific with your shares. I will get to exactly when. For a long time I assumed a transfer agent was one of those grown-up things every company just has, like a registered agent or a payroll provider. That is not how it works.

This is the same move we made with our SOC 2 compliance stack. Look hard at what the vendor does. Keep the part that carries legal weight. Run the rest yourself, with AI on the boring bits.

What a transfer agent does

Let me start with the job, because most founders (me, a few years ago, included) muddle two different things.

A transfer agent is a regulated record-keeper. The SEC’s own description is plain: a transfer agent will record changes of ownership, keep the issuer’s security-holder records, cancel and issue certificates, and pay out dividends. They are usually a bank or a trust company, and they must register with the SEC or a banking regulator to do the work. That registration is the whole point. For a public company with shares changing hands every second, you want a neutral, regulated party tracking who owns what.

Cap-table software is a different animal. Carta and Pulley, the two names everyone reaches for, are not transfer agents in the default case. They keep your ledger in their cloud, model dilution, run 409A coordination, and produce reports. Useful. Also a subscription that grows with your stakeholder count. The mix-up between “transfer agent” and “cap-table tool” is the elephant in the room, and the vendors are not in a rush to clear it up.

Then there is the third option: keep the record yourself and let AI do the clerical work. Here is how the three compare.

| What it does | Transfer agent | Cap-table software | Founder DIY + AI |

|---|---|---|---|

| The record of truth | Holds it for you | Holds it in their cloud | You hold it (JSON in Git) |

| Issue or cancel shares | Yes, on your behalf | Yes, in-app | Board resolution, then a line in the ledger |

| Stock ledger (DGCL 219) | Maintained for you | Maintained in-app | Maintained by you, version-controlled |

| Reconciliation and checks | Manual or a service | Built-in dashboards | A script plus an AI cross-check |

| Cap-table reports, 409A exports | Add-on service | Yes | AI-generated from the JSON |

| Reminders for filings | Service | Yes | Cron job or a calendar |

| Cost | Highest | Subscription | Your time plus cents of AI |

| Legally required? | Only in specific cases | No | No |

| Who makes the legal call | Your counsel | Your counsel | Your counsel |

Notice the bottom rows. Two of the three are not required by anyone, and all three lean on the same human: your lawyer. The software does not do your compliance any more than a folder does. It organizes it.

Do you even need one?

For most private companies, no. insightsoftware put it bluntly: most private companies do not need a transfer agent at all. The interesting part is why the law agrees.

Three pieces of Delaware law do the heavy lifting. A Delaware corporation can issue uncertificated shares the moment the board passes a resolution, so there is no paper certificate to chase. The company’s stock ledger, under DGCL Section 219, is the corporation’s own record, and the statute calls it “the only evidence as to who are the stockholders entitled … to vote.” Your record. Not a vendor’s. And DGCL Section 224 says those records, the stock ledger included, may be kept “by means of … 1 or more electronic networks or databases,” distributed ones included, as long as they convert to clear paper in a reasonable time. That language is not an accident. The Council of the Corporation Law Section of the Delaware bar pushed the 2017 amendments precisely so companies could keep ledgers on databases. The state told you, in writing, that a database is a legal stock ledger.

OK, so when does the picture change? The trigger lives in the Securities Exchange Act. Under Section 12(g), a company has to register once it crosses 10 million dollars in assets and has a class of equity held of record by 2,000 people, or 500 who are not accredited investors. My guess is most companies never sniff that line, certainly not before a Series C. And a subtlety that trips people up: a SAFE or a convertible note is not a class of equity security. It is a contract that might become stock later. So the angels and the crowd who came in on SAFEs are not holders of record of your stock. Your stockholder list stays short.

Does that make a transfer agent a waste of money? No. There are real cases where you want a registered one. Going public is the obvious case. So is a Regulation A+ Tier 2 raise, where the SEC requires a registered transfer agent as a condition. And here is the one that catches crowdfunded startups: if you ran a Regulation Crowdfunding round and want those investors to drop out of the Section 12(g) headcount, Rule 12g-6 lets you, but only if you stay current on your Reg CF reports, keep assets under 25 million dollars, and engage a registered transfer agent. So the crowdfunding case is exactly where the “you don’t need one” rule gets a sharp asterisk. This is YMYL territory, so I will say it plainly: talk to a securities lawyer about your facts.

How we run ours with AI

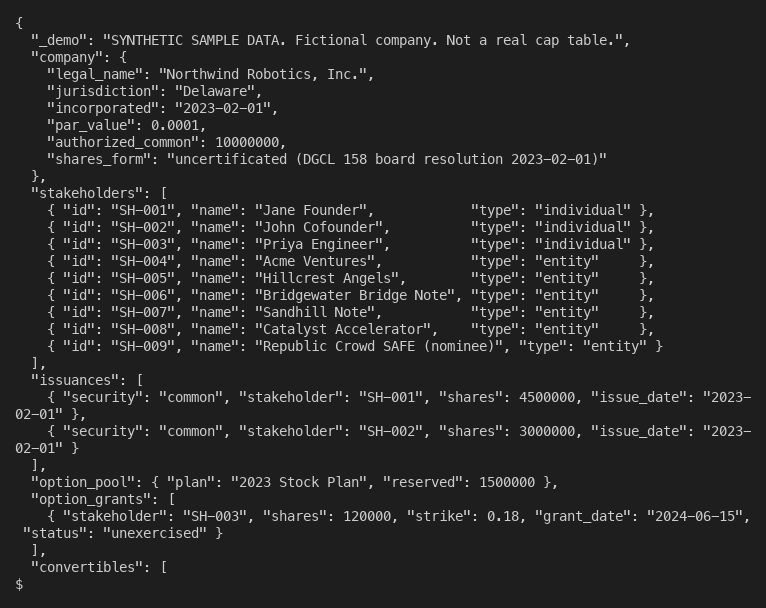

The shape of ours is boring on purpose. One JSON file is the source of truth, structured loosely along the lines of the Open Cap Table format. It lives in Git, mirrored to Dropbox, so every change has an author, a timestamp, and a diff. That alone beats most platform activity logs, the same way version control gave us a free audit trail for compliance. The alternative most founders cobble together (a spreadsheet, a reminder app, and a vendor login that nobody checks) is the thing that actually drifts.

The cap table as one JSON file, version-controlled in Git. Synthetic sample data, not our real ledger.

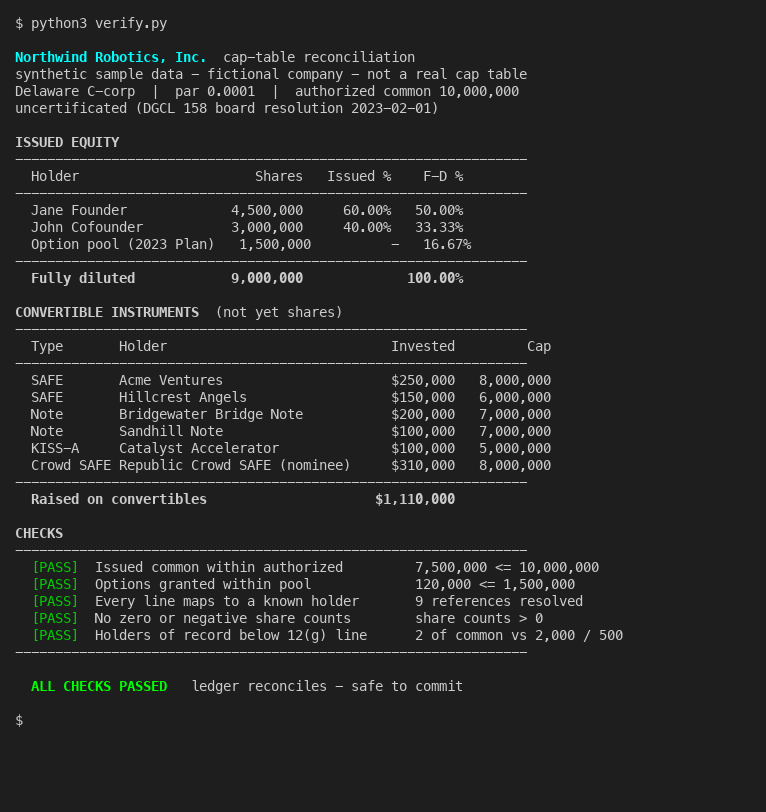

A short script reads that file and checks the arithmetic. Issued shares against authorized. Options granted against the pool. Every line tied to a real stakeholder. Holders of record against the Section 12(g) line, so we get a nudge long before it matters. It prints a pass or a fail. This is it, running on a fictional company so I can show you the workflow without showing you ours.

One script reconciles the whole ledger and prints pass or fail. Synthetic data. The green line at the bottom is the part that lets me sleep.

AI is where the operations work I hand to Claude lives. Claude reads the JSON and produces the stockholder list the statute wants, the ownership tables, a dilution model for a hypothetical priced round, a draft Form D, the lot. They come out as board-ready artifacts. Claude cross-checks the numbers and flags anything that does not tie out.

This is the same pattern I have written about for running real work through Claude Code and for self-driving workflows: the model does the reading, cross-referencing, and drafting; a human applies judgment. It behaves more like a careful clerk than like rigid RPA, which would choke the first time the data looked slightly off.

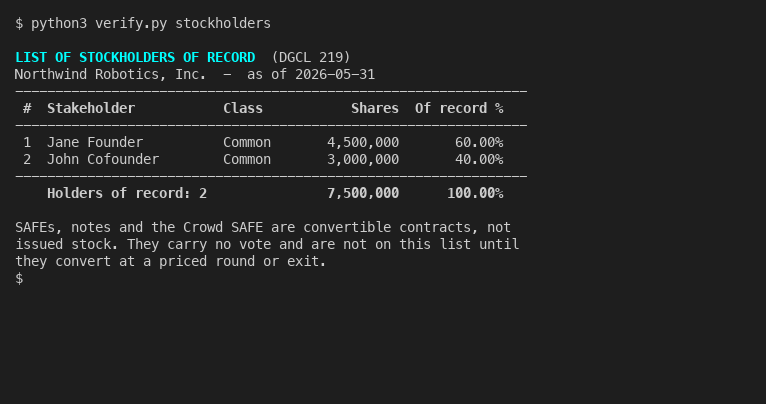

The Section 219 stockholder list. Two holders of record. The SAFEs and the Crowd SAFE are contracts, not stock, so they are not on it yet.

For context, our real table is the usual early-stage spread: founder common stock, employee option grants, a handful of angel SAFEs, a couple of convertible notes, an accelerator’s KISS-A, and a Republic Crowd SAFE round where the crowd sits behind a single nominee line. Plenty of instruments. Few holders of actual stock. AI is good at exactly this sort of cross-referencing, whilst a human and our counsel sign off on anything that moves the legal picture: a new issuance, a conversion, a board consent.

I keep calling these scripts simple. Wrong word. They are not clever, and that is the point. A cap table should be dull. The moment it gets interesting, something has usually gone wrong.

Hand it off when these are true

I would rather tell you where this breaks than sell you a clean story.

Hand it to a transfer agent or a lawyer when your securities get messy. Cap tables suffer scope creep like everything else: clean at incorporation, a tangle three rounds later, with warrants, secondary transfers, side letters, and a pile of option exercises. A mistake on a real stock ledger has consequences. If you are heading for an IPO, hand it off anyway, because you will need a registered transfer agent regardless. Cross the Section 12(g) or Reg CF thresholds above, and the same applies. And if nobody on your team will own the discipline of keeping the ledger current, pay someone, because a ledger that drifts is worse than no ledger.

If keeping a tidy record sounds like a nightmare rather than a Tuesday, that is a fair reason to pay for one. No shame in it. The point is that you are choosing, not defaulting into a subscription because everyone else has one.

What it costs, roughly

Money is where this gets stark. A transfer agent for a private company runs into the thousands a year, and some charge you a fee on the way out. The same writeup notes the obvious point: those fees dwarf a software subscription. Cap-table software costs less than that, a subscription that grows with how many stakeholders you carry. Running it yourself costs your time plus a few cents of AI per reconciliation.

So the trade is fees for your own time and a bit of discipline. For a five-person company that already lives in Git, that is a no-brainer. For a company with a finance team and a hundred holders, paying for the tidy interface and the reminders might be the right call. We landed on the do-it-yourself side because we already had the muscle: version control and AI in the workflow, plus the patience to keep a ledger straight.

None of this is legal advice. Securities and corporate law turn on your jurisdiction and your specific facts, and we run a Delaware C-corp and talk to our counsel before we touch anything that matters. You should too. If you want a second pair of eyes on whether your structure is simple enough to run this way, that is the sort of back-office problem I take on through Blue Sheen.

One thing stuck with me. The stock ledger is a list of who owns what. Delaware has said for years, in the statute itself, that the list can live in a database. The transfer agent and the platform were never selling you the list. They were selling you the feeling that keeping it was hard. Once AI does the dull part, that feeling is worth a lot less than the invoice.

More: putting AI on real company jobs

This is one of a run of posts on back-office work you can hand to AI instead of renting a vendor for it:

- Replacing a SOC 2 compliance platform with AI and Google Drive - the same idea, applied to security compliance and auditors.

- AI does tasks, not jobs - why this works for clerical tasks and where it stops.

- The fractional AI executive - putting AI on judgment-heavy functions, not only clerical ones.

- Claude for operations - the day-to-day version of this across an ops team.

- Knowledge management with Claude Projects - keeping a company’s records as one living source of truth, the same instinct as the ledger here.

- When AI replaces knowledge workers - the bigger pattern behind all of it.